Imagine two scenarios:

- Ted works in the information technology department. He has always been seen as extremely helpful. Employees would call help to help set up a computer or fix a problem. Lately, it’s taking Ted longer and longer to arrive to help. When he does, he’s very stressed and hurried. Ted’s company has hired many new people in the past few weeks and plans to continue to hire more.

- Bella’s Bikes makes high-end bicycles. One step of the process is to powder-coat the bike with paint. The frame is put in an oven to cure the paint. Sales are booming. The new budget added additional sales staff and an aggressive pricing strategy. Bella’s production facility has been producing bicycles as fast as they can. The paint oven is constantly running. Yet, bicycle frames are starting to pile up in front of the paint booth and oven. Dozens of frames are waiting to be painted.

Both of these scenarios are examples of unanticipated capacity constraints. The solution is an increase in a step fixed cost, also known as a step cost.

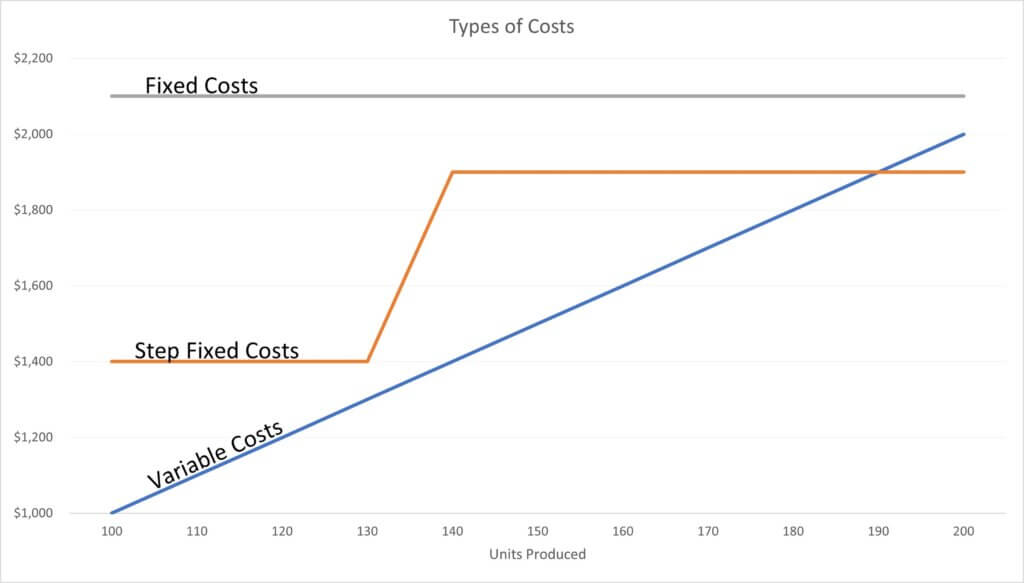

What are step costs? A step cost is a cost that stays fixed over a range of production but then shifts to another level of fixed cost when production goes above or below that range. They are called step costs because they look like steps when graphed. Below is a graph of fixed, variable, and step costs.

The graph below shows the three types of costs. Fixed costs are a straight horizontal line regardless of the volume produced. Variable costs are an upward-sloping straight line. Step costs are a horizontal line that jumps to another level at around 130 units.

In the two example scenarios, hiring another IT person and buying another powder coat oven are both step costs. Each person or oven has a capacity for what they can process. Those companies have two choices:

- Limit their production to the capacity of that step cost

- Invest in another step to expand capacity for more production.

The situation at Bella’s Bikes is especially problematic because it represents a bottleneck. A bottleneck is a point in a process that limits the process’s production (i.e., throughput). Bella can build all the frames she wants, but they will just pile up in front of the oven, waiting to be painted and cured.

Identifying bottlenecks and increasing their capacity (i.e., exploiting them) is an important process management task. The classic book on this is The Goal by Eliyahu Goldratt. I read it 30 years ago, and it’s been important throughout my career.

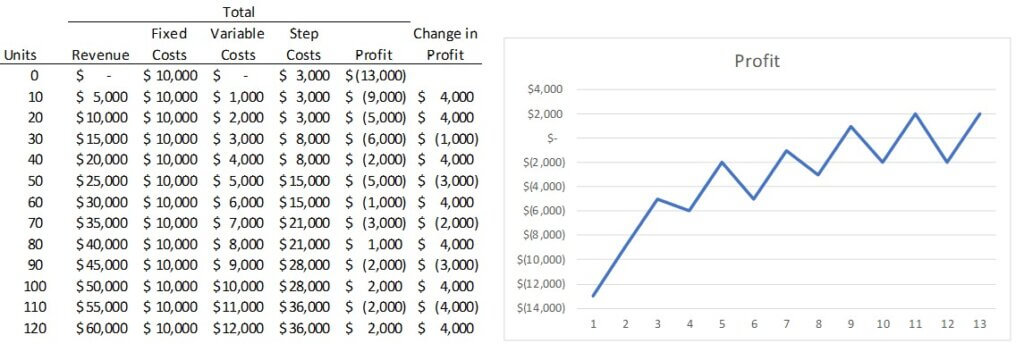

Step costs create varying amounts of profit over the range of production for which they don’t change. Profit quickly increases as the excess capacity purchased from the last step cost investment is increasingly utilized. Crossing a production threshold that requires another step cost investment can cause profits to dive again.

The graph below shows profit across a series of step costs. The smooth upward-sloping profit line we saw when only looking at variable costs is now a saw blade.

One of the biggest budgeting mistakes I’ve repeatedly run into is overestimating the capacity of a step cost. Most of the time, the step cost’s capacity isn’t just overestimated; it’s not even considered. This leads to massive unanticipated costs that create big budget variances. Profitability drops as we fall from the last peak of full utilization because we had to make another step cost.

This loops all the way back to budgeting units of production, not just the cost of goods sold. Capacity is measured in units, not dollars. You must know the capacity of each process and person/team. If your budget exceeds this, you then calculate the cost to increase capacity and add it to the budget. Choosing how much capacity to add (i.e., how large of a step to take) and at what cost is a management decision. Another option is to reduce budgeted production to current capacity.

Knowing capacity also allows you to utilize excess capacity. This is often highly profitable.

There’s a joke that goes, “An optimist will tell you the glass is half-full; the pessimist, half-empty; and the engineer will tell you the glass is twice the size it needs to be.” Look at processes like that engineer to assess capacity. If demand exceeds capacity, estimate the step fixed cost to increase capacity and decide if it’s worth the investment.

To learn more about budgeting analysis, check out my Better Budgeting course.

For more info, check out these topics pages: